Saturday, 6 August 2016

Wednesday, 27 July 2016

producer's equilibrium

meaning of producer.

producer is a person who produces goods and services for sale and his objective is profit maximization.

Q2 define producer's equilibrium

Ans. the word equilibrium in economics has been taken from physics where it means, state of rest. but in economics it is used in different sense. so, producer's equilibrium is a situation where producer is in best possible situation. for eg. : if a producer gets maximum profits than he will in equilibrium where as in the situation of losses he gets minimum losses then producer is said to be in equilibrium and here he has no tendency to move away from the equilibrium situation.

Q3. what are various approaches to determine producer's equilibrium.

Ans. there are two approaches to determine producer's equilibrium:

i) TR and TC approach

ii) MR and MC approach

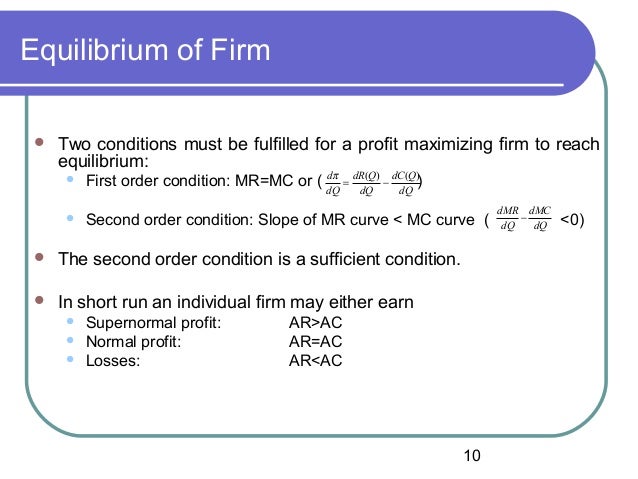

Q4 explain the producer's equilibrium with the help of MR and MC approach?

or

what is the general profit maximization condition of a firm?

or

show that a perfectly competitive firm maximizes its profit only when price = MC?

i) when MR is in straight line or P.E. under perfect competition :-

A producer is said to be in equilibrium when given level of output gives him maximum profit and he has no intention to change the level of output . with a view to maximise his profits, a produce upto that quantity at which following two conditions are fulfilled.

MC = MR MC cuts MR from below.

output MR MC

1 10 8

2 10 7

3 10 6

4 10 8

5 10 10

6 10 13

the table is drawn on the assumption that price (AR) is constant so MR is constant (10) we are assuming a situation of perfect competition. the table shows that two conditions are satisfied only when 5 units are produce :-

i) MR = MC

ii) MC, is cutting MR from Below. (MC is rising )

the producer's equilibrium can be explained with the help of table and diagram.

we consider equilibrium of a producer who is working under conditions of perfect competition and takes the price of the product as given and constant for him.

condition - I MC = MR

if the producer produces OM units, he can increase profits of the firm = T as MR = MC MC cuts MR from its below thus he want to increase production to OS, so as it earn maximum profits.

if on the other hand, the producer produces 400 units, then he suffers losses = after point T as MC >MR, so the producer will prefer to produce till 350 units, where MC = MR, MR is rising and profit maximum.

condition-2 MC is rising

in the diagram MC curve cuts MR curve at point K and T. at point K , firm produces OM units of output, as the firm increase its output from OR units of output, as the firm increases its output from OR to OQ initially its MC will go to falling but MC is less than MR it means productions from OR to OQ will add to the profits of the firm.

this point K cannot be the point of equilibrium of the firms thus point E represent producer's equilibrium as at this point MC = MR and MC is rising.

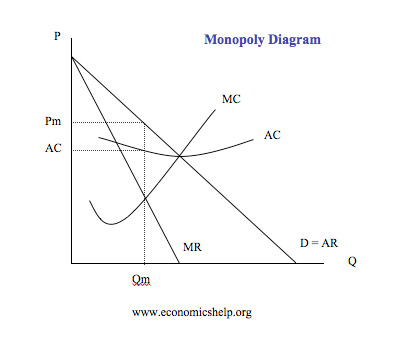

Q5 explain producer's equilibrium with MC and MR method under imperfect competition?

Ans- ii) when MR curve is downward sloping

according to this approach a producer will be in equilibrium when following two conditions are satisfied.

i) MC = MR

ii) MC cuts MR from below

i) MC = MR

MC = MR and MC is cutting MR from below, so here a producer will be in equilibrium.

ii) MR > MC

MR > MC, so here a firm will get profits. therefore a producer will increase output.

Q6 explain the determination of short run equilibrium of the firm under perfect competition?

Ans- producer's equilibrium - short period and long period analysis

short period :-

it is a time period in which new firms cannot join the industry and existing firm cannot leave the industry.

in short period a firm or producer will be in equilibrium when following two conditions are satisfied

i) MC = MR

ii) MC, uts MR from below

in short period firm may have to face following three situations.

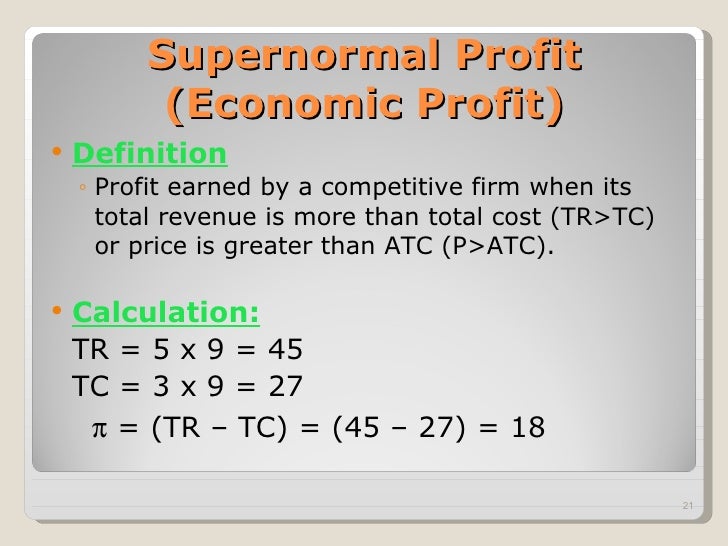

1. super normal profits or abnormal profits or extra normal profits :-

a firm will get super normal profits when price becomes greater than AC . or when TR >TC.

2. normal profits or zero abnormal profits:-

a firm will get normal profits when price becomes equal to AC. TR = TC.

3.abnormal losses or extra normal losses:-

a firm will get losses when AC becomes greater than price. TR <TC.

AR < AC

Q8- what is shut down point ?

Ans- shut down point

it is the point where price becomes equal to AVC

price = AVC , so it is called shut down point.

gross profits = TR - TVC

net profits = TR - TC

Q9- only a rising segment of MC curve starting from the shut down point is considered as a short period supply curve of a firm. explain/

Ans- a competitive firm strikes its equilibrium, when at a given price, MR = MC and MC is rising. during the short period a firm will undertake production only if AR or P > AVC i.e. a short period supply curve of the firm starts from its shut down point, where P = AVC starting run supply curve would be the same as its MC curve which shows the price + quantity relationship.

In the diagram, the firm is in equilibrium where MR = MC and MC is rising.

P = AVC ( shut down point ) which is the starting point of firm's supply curve producing OQ quantity. when price increases the firm strikes equilibrium , and the firm produces OQ1 quantity. thus during the short period, rising segment of MC curve ( starting from the shut down point ) is the same as the firm's supply curve as it shows positive relationship between price and quantity supplied.

Q11. the break even point and shut down points are different how?

Ans. break even point occurs when the firm's total revenue is equal to the total cost i.e. no profit no lose situation.

TR = TC or AR = AC

shut down point is the point at which the market price of the product is equal to the AVC. fixed costs are not recovered at this point. the firm continuous production till this point as at least the variable costs is being recovered.

TR = TVC or AR = AVC

\

Wednesday, 13 July 2016

concepts of revenue

meaning of revenue or sale proceed

by selling the commodity what ever money is received by the firm is called revenue.

suppose you are running a factory producing chocolates. you produce 1000 chocolates daily. by selling these chocolates you get RS 2,000. in economics , this amount of rs 2,000 is called revenue. thus, by selling a commodity whatever money a firm receives is called revenue.

or

revenue is the money received from sale of commodity.

difference between revenue and profits?

revenue and profits are different concepts

the concept of revenue is different from the concept of profit .

the following equations shows the difference:-

profit = revenue - cost

revenue = costs + profit

concepts of revenue

i) TR ( total revenue)

ii)AR (average revenue)

iii)MR (marginal revenue)

i) total revenue (TR) :-

a revenue that a firms get by selling a given amount of output that is called total revenue.

TR = P*Q

TR = TOTAL REVENUE

P = PRICE PER UNIT

Q = QUANTITY SOLD

or

TR =SUMMATION OF MR

TR = TOTAL REVENUE

MR = MARGINAL REVENUE

marginal revenue ( MR)

it is change in total revenue as a result of selling an additional unit of output is known as marginal revenue. however it can be positive, zero nd negative.

MRn =TRn - TRn-1

MRn = marginal revenue of n units

TRn = total revenue of n units

TRn-1 = total revenue of n-1 units

or

example

P Q TR = P*Q MR

5 1 5 5

4 2 8 3

3 3 9 1

2 4 8 -1

1 5 5 -3

MR2 =TR2 - TR1

= 8 - 5

= 3

average rvenue

it is the revenue per unit of output. it is obtained by dividing T. R with the quantity sold . AR is equal to price.

AR = Average revenue

TR = Quantity sold

Q TR AR = TR/Q

1 10 10

2 20 10

3 30 10

4 40 10

Q4 show that AR = price ?

Ans. we know that

AR = TR/Q

we also known that TR = P ( where P = quantity or output sold)

relating the two equations we write that;

AR = P*Q/Q = P

thus it is proved that AR = price

Q5 Firm's demand curve or price line is the same as AR curve ?

ans. firm's demand curve or price line is the same as firm's AR curve, because AR means price\, and demand curve ( or Ar curve ) shows the relationship between price and quantity demanded of firm's output.

Q^ what is relationship between TR, AR and MR under perfect competition ?

Ans. perfect competition is a market in which there are large number of buyers and sellers where as in this market product produce is homogonous and there is free entry and exit of firms .

in such a market price of commodity is determined by industry and firm followed that price A firm can sell any amount of commodity at this price.

price Q TR = P*Q MR AR = TR/Q

10 1 10 10 10

10 2 20 10 10

10 3 30 10 10

10 4 40 10 10

10 5 50 10 10

!. it is clear from diagram MR is constant so TR is increasing at constant rate therefore TR is in a straight line moving upward.

2. AR and MR are equal to each other and it is shown by horizontal straight line where as AR = MR because industry is a pric maker and firm is price taker.

Q7 prove that area under AR & MR curve is equal to Tr in case of perfect competition ?

Ans. in case of perfect competition AR is constant therefore AR = MR. AR curve is horizontal line which represents the value of different level of output at uniform prove.

in the diagram, price ( equal to OP) is constant and output is equal to OQ.

TR = P*Q

= OP*OQ

Area = OPRQ

Q8. what is relationship between TR,AR and MR?

Ans. the relationship between TR,AR and MR can be explained with the help of diagram.

p Q TR MR AR

10 1 10 10 10

9 2 18 8 9

8 3 24 6 8

7 4 28 4 7

6 5 30 2 6

5 6 30 0 5

4 7 28 -2 4

3 8 24 -4 3

2 9 18 -6 2

1 10 10 -8 1

1. when MR is positive then TR is increasing as in the diagram upto point K, MR is positive. so, TR is increasing upto point E1.

2. when MR is zero then TR is maximum as in the diagram at point K, MR is 0 and TR is maximum at point K'

3. when MR is negative then, TR is falling as after point k, MR is negative and TR is falling. after point K'.

4. both AR and MR are decreasing but MR is falling at faster rate. so, MR is below than the AR.

5. MR can be negative but TR and MR cannot be.

6. both TR ad MR can be calculated from TR.

(a) MR = TRn - TRn-1

(b)AR = TR/Q

Q9 can MR be zero or negative ?

Ans. Yes, MR can be zero or negative. it is clear from the following illustrations;

Average revenue output (units) total revenue marginal

price (Rs.) (Rs.) revenue (Rs.)

100 1 100 100

80 2 160 60

40 3 160 0

30 4 150 -10

1. MR can be zero or even negative, but only when price is declining as under monopoly or monopolistic competition.

2. TR stops increasing when MR = 0 so that TR is maximum when MR = 0.

3. TR starts declining, less and less added to TR is every additional unit is sold. accordingly, TR increases only at the diminishing rate.

Q10 what is firm's price line/ what is its shape?

Ans. firm's price line is the same as firm's AR curve. under perfect competition, firm's price line is a horizontal straight line. both AR and MR tend to coincide (AR=MR). under monopoly or monopolistic competition, firm's price line slopes downward. when AR sloped downward, MR also slopes downward, MR<AR.

Tuesday, 12 July 2016

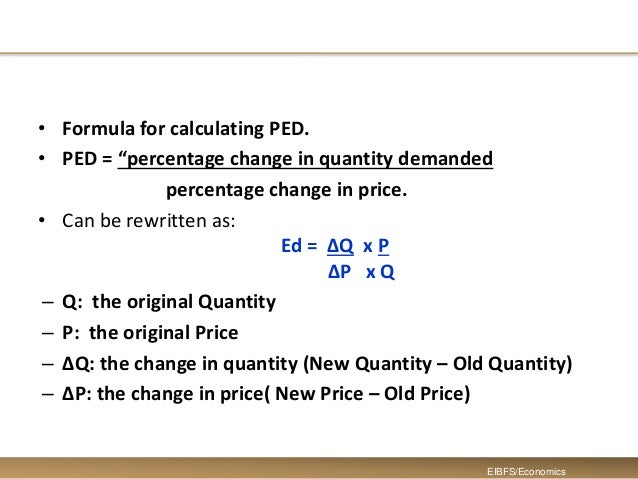

price elasticity of demand

introduction of elasticity of demand

law of demand tells us that with the increase in price demand falls and with the fall in price demand increases. it does not tell about how much is the change in the demand due to change in price. elasticity of demand tells us about how much is the change in demand due to change in price, income and price of related goods.

meaning of elasticity

it means responsiveness of a dependent variable to change in independent variable.

or

it refers to the % change in qty. demanded and % change in own price of the commodity.

meaning of elasticity of demand

it is the demand which is affected by 3 factors.

i) price :- when demand changes due to change in the price of the commodity is called price elasticity of demand.

ii) income :- when demand changes due to change in income of the consumer i.e. called income elasticity of demand.

iii) related goods :- when there is change in demand due to change in price of related goods that is called cross elasticity of demand.

price elasticity of demand :-

the ratio of % change in demand due to % change in price i.e. called price elasticity of demand

degrees/types/kinds/ of price elasticity of demand

there as 5 degrees of price elasticity of demand.

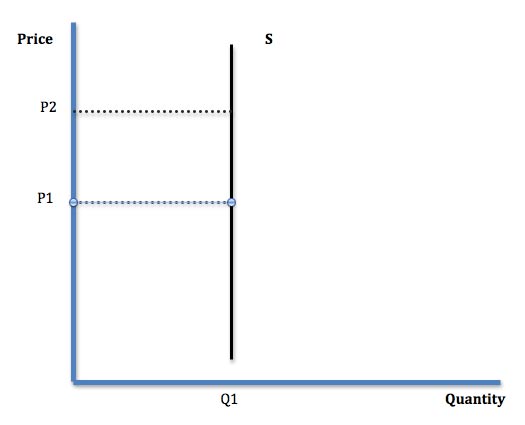

i) perfectly inelastic demand or zero elasticity of demand :-

when there is no change in demand due to change in price of commodity i.e. called perfectly, inelastic demand for e.g. salt, life, saving, drugs.

price demand

10 10

11 10

12 10

13 10

14 10

15 10

it is clear from the diagram that demand curve is parallel to or vertical line to 'y' axis i.e. there is no change in demand due to change in price. so here ed is equal to zero. it is known as completely or totally inelastic demand.

ii) less elastic demand or inelastic demand or less than unitary elastic demand :-

when % change in price is greater than % change in demand than elasticity of demand is less than unitary elastic demand ex. food, fuel etc.

price demand

10 10

5 11

it is clear from the table that price falls by 5 Rs demand increases by 1 unit. this ed is said to be less than one.

it is clear from the diagram % change in price PP1 is > than % change in demand QQ1 i.e. why elasticity of demand is less than unitary elastic demand. the shape of demand curve is steeper.

iii) unitary elastic demand

when % change in price is equal to % change in demand than elasticity of demand is unitary elastic demand for e.g. clothes, normal goods.

price demand

10 10

9 11

it is clear from the table that price falls by 1 Rs and demand increases by 1 unit. the ed is said to be unitary elastic.

it is clear from the diagram that % change in price PP1 is equal to % change in demand QQ1 so elasticity f demand is unitary. in this case area covered by each rectangle is equal so it takes the shape of rectangular hyperbola.

iv) greater than unitary elastic demand or elastic demand ;-

when % change in demand is greater than % change in price than elasticity is greater than unitary elastic demand. for example luxuries ( costly cars, costly carpets).

price demand

10 10

9 15

it is clear from the table price falls by 1 Rs and demand increases by 5 units. so ed said to be more elastic.

it is clear from the diagram that % change in demand QQ1 is greater than % change in price PP1 so elasticity of demand is greater than unitary elastic demand. the shape of demand curve is flatter.

v) perfectly elastic demand or infinite elasticity of demand :-

when demand is infinite at the existing price than elasticity of demand is perfectly elastic in real world we never come across such type of elasticity of demand.

price demand

10 10

10 11

10 12

10 13

10 14

here elasticity of demand becomes infinite and demand curve is 11 to 'x' axis. this type is an imaginary elasticity of demand so it does not exits in real world.

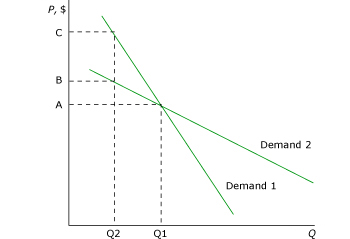

Q- when two demand curves intersect each other which is having greater elasticity of demand?

Ans - if 2 demand curves intersect each other than flatter demand curve is having greater elasticity of demand.

it is clear from the diagram that d1d1 and d2d2 are intersecting each other at point 'a' at this point price is op and qty. demanded for both the demand curve is Q2. if price falls from OB to OA the change in price is same for both the demand curves but change in Qty. demanded is different. on DD demand has increased from OQ2 to OQ1 where as for demand curve D1D1 demand has increased for OQ2 to OQ1. it is clear that % change in demand for flatter demand curve is more so elasticity of demand for flatter demand curve is more.

methods to measure PED

the following are the methods to measure price elasticity of demand

1. % method or proportionate method

2. total expenditure method or total outlay method

3. point method or graphic method

1) proportionate method or percentage method

this method was given by Dr . marshall.

according to this method elasticity of demand is the ratio of % change in demand to % change in price.

price demand

P 1 5 Q

P1 5 4 Q1

total expenditure or total outlay method

this method is given by Dr. Marshall. it works out relationship between PED and TE. this method measured PED by finding out how much and in what direction the total expenditure changed in price of the good.

according to this method total expenditure can be calculated by multiplying price per unit with qty. sold.

T.E. = P * Q

P = price per unit Q = quantity sold

according to this method there are 3 degrees of price elasticity of demand.

i) less than unitary elastic demand

ii) unitary elastic demand

iii) greater than unitary elastic demand

i) less than unitary elastic demand

when there is positive relation between price and T.E. that is with the increase in price total expenditure increase and with the decrease in price T.E. decrease.

P increases T.E increases

P decreases T.E. decreases E < 1

ii) unitary elastic demand :-

when there is no change in T.E. due to change in price is called unitary elastic demand.

price increases or decreases T.E. same E = 1

iii) greater than unitary elastic demand

when there is inverse relationship between price and T.E. that is called greater than unitary elastic demand.

price increases T.E. decreases

price decreases T.E. increases E > 1

P Q T.E. change in P PED

& TE

10 1 10

9 2 18 Price increases T.E. greater

8 3 24 increases E > 1 than one

7 4 28

6 5 30 price increases T.E. unit

5 6 30 same E = 1

4 7 28 price increases T.E. less than

3 8 24 decreases E < 1 one

note :- the relationship between P & TE based on inverse relationship between P & Q .

1. it is clear from the diagram when price falls from OP to OP1 total expenditure increases from PT to P1T1 so here elasticity of demand is greater than one.

2. when price falls from OP1 to OP2 T.E. remains the same i.e. P1T1 = P2T2 so here E = 1

3. when price falls from OP2 to OP3 T.E. falls from P2T2 to P3T3 so here elasticity of demand is E<1

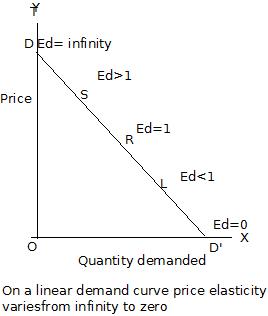

point method / graphic method / geometric method

it was given by Dr. Marshall. this method is used to measure price elasticity of demand on the different points of demand curve. this method measures elasticity graphically. this method is called graphic method. According to this method following formula is used

i) elasticity of demand at the mid point of demand curve or PED = 1 :-

at the mid point of demand curve lower portion is equal to upper portion. so here elasticity of demand is unitary elastic demand.

ED at Pt A = AL

AP

AL = AP

ED = 1

ii) elasticity of demand below the mid point of demand curve PED<1 :-

in this situation lower portion is lesser than upper portion so here elasticity will be less than unitary elastic.

Ed at Pt B = BL

BP

BL<BP

ED < 1

iii) elasticity of demand above the mid point of demand curve or PED>1 :-

in this situation upper portion is less than lower portion so here elasticity of demand will be more than unitary elastic.

ED at Pt C = CL

CP

CP<CL

ED > 1

iv) elasticity of demand when demand curve touches 'x' axis or PED = 0 :-

in this situation elasticity of demand will be equal to zero.

Ed at Pt L = O

PL = 0

v) elasticity when demand curve touches Y axis or PED = infinity :-

in this situation elasticity of demand will be infinite.

Ed at Pt P = PL

O = infinity

Q- the demand curve of a commodity is a straight line sloping downward as in the diagram. write true or false against the following statements :-

i) elasticity of demand is low corresponding to lower level of price of the commodity.

ii) elasticity of demand = 0, when price = 0.

iii) elasticity of demand at point 'D' < elasticity of demand at point 'C'

Ans - the statement is true.

at a lower level of price, lower segment tends to decrease while upper segment tends to increase. implying that elasticity of demand reduces as price tends to be lower than before.

ii) the statement is true.

price = 0, at point B,

Ed at point B = O

AB = 0

Elasticity of demand = 0, when price = 0.

iii) the statement is true . because

elasticity of demand at point D is less than elasticity of demand at point c.

Q- find own price elasticity of demand when 5 percent increase in price causes 5 percent increase in expenditure on the commodity.

Ans- it is a situation of zero own price elasticity of demand. because expenditure on the commodity is increasing proportionate to increase in price, so that total purchase of the commodity remains constant. constant purchase means zero elasticity of demand.

Q- why is demand for water inelastic?

Ans- demand for water is inelastic, as water is an essential of life.

imp. factors affecting price elasticity of demand

1. nature of commodity :- by nature of commodity demand

A) necessities of life :- the goods which are necessities have inelastic demand i.e. there demand is not much affected by price. for e.g. wheat, salt, vegetables, etc.

B) luxuries :-

the goods which are luxuries such as important cars fashionable garments costly furniture, AC etc. have elastic demand because their demand is much affected by price.

C) comforts :- the goods that are comforts to the life for e.g. fans, refrigerator etc. have neither very elastic nor inelastic demand.

D) jointly demanded goods :- like bread and butter, pen and ink show a moderate elasticity of demand.

2. availability of close substitutes :-

the goods whose substitutes are available such as pepsi and coke have elastic demand where as goods whose sub are not available such as cigarettes, liquor etc. have inelastic demand.

3. different uses of commodity or diversity of uses :-

the goods which can be put to verity of uses have elastic demand for e.g. electricity, milk etc. if there price falls there demand increases much because people start using it in very less important uses. on the other hand if a commodity such as paper has only few uses, its demand is likely to be less elastic.

4. income of the consumer :-

the goods that are consumed by very high and very low income group people have inelastic demand. where as middle income group have elastic demand. for ex. demand of small cars by middle income group is elastic. where as demand of luxury cars is inelastic.

5. price level :-

if the price of a commodity is high its demand will be elastic and if price of commodity is very low then its demand is inelastic.

6. postponement of the use :-

the demand will be elastic for those commodities whose consumption can be postponed and vice - versa. such as demand of residential houses. people often defer their demand for residential houses when interest rates on loans are high.

7. habit of consumer :-

the goods to which a consumer become habitual have inelastic demand such as cigarette, liquor etc. because a person cannot live without them. on the other hand demand of cigarettes, liquor does not reduce even when these goods are heavily taxed.

importance of price elasticity of demand

I) useful to a producer :-

every producer aims at maximizing his profits by promoting his sales. to increase the sales he reduces the price of more elastic goods and charges high price for less elastic goods .

II) useful to finance minister :-

the finance minister makes the use elasticity of demand by imposing taxes in the budget he fixes more taxes on inelastic commodities and less taxes on elastic commodities.

III) importance in factor prices :-

if demand for factor price is inelastic than a factor will get high wages where as a factor will get lesser wages if demand for factors is more elastic.

IV) importance in international trade :-

it helps to determine trade between two countries. a country fixes more prices of the product whose demand is inelastic where as less price of the product whose demand is elastic.

v) useful to monopolist :-

for the monopolist the knowledge of elasticity of demand is essential. a monopolist will fix high price for those goods whose demand is inelastic less price for those goods whose demand is elastic.

Monday, 6 June 2016

theory of demand

desire

it means wish of a person to have a commodity but doesn't have enough money to buy a commodity e.g. if a consumer wants to buy a color T.V. but he is not having money to buy it i.e. desire.

want:-

it means desire to have a commodity and also have enough money to buy a commodity but not ready to spend it .

example:- if a person wants to buy a color T.V. and he is having money to buy it but he is not ready to spend it on color T.V. i.e. want .

demand

the demand for a particular good refers to desire to buy a commodity backed with sufficient purchasing power and willingness to spend .

example :-A consumer demand a color T.V. in a month at price of rs 20,000.

conditions for demand to take place or elements of demand

1. desire for the good

2.purchasing power to buy the good

3.readiness to spend the money

4.availability of the good in the market at particular price at particular time.

Q:-what do you understand by quantity demanded?

Ans it refers to the specific amount of quantity to be purchased against specific price of the commodity e.g. demand for the commodity x refers to 10 units of x if px =5, 8 units x if Px =6

quantity demanded of a commodity x refers to 8 units of 'x' if px= 6 Rs

demand function or factors influencing demand or determinants of demand

A demand function explains the relationship between the demand for a commodity and the factors affecting demand . these factors are also called determinant of demand. they are:

Dx=f [px, Y, T, ..., ..]

1. prices if the commodity itself (p)

2.income of the consumer (y)

3.taste, preference and fashion [T]

4.size and composition of population (N)

5.price of the related commodity (PR)

6.expected price [E]

7.distribution of income (yd)

1. PRICE OF THE COMMODITY ITSELF(P):

there is an inverse relationship between the price of the commodity and the quantity demanded. it means, generally with rise in price, quantity demanded falls and vice-versa also

2. INCOME OF THE CONSUMER (Y):

Income of the consumer affects demand for normal goods and inferior goods in different ways. both cases can be discussed as follows :

in case of normal goods as income increases demand increases as income decreases demand decreases.

in case of inferior goods as income increases demand decreases and vice versa

3. CHANGE IN PRICE OF RELATED GOODS (PR):

there are two types of related goods.

i) substitute goods :- those goods which can be used in place of one another are known as substitute goods. Ex. tea and coffee, Reynolds and Rotomac, Pepsi and coke, fountain pen and ball pen.

in case of substitute goods as price of (x) goods increases demand of (Y) good increases . as price of Pepsi increases demand of coke increases.

ii) complementary goods:

those goods which cannot be used in absence of one another are known as complementary goods or those goods which are used together to satisfy a particular demand are called complementary goods. Ex. bike and petrol, ink and pen, camera and roll, tea and sugar, cell phone and battery etc.

in case of complementary goods as price of (X) increases demand of (Y) good decreases. as price of petrol will increases demand of bike will decreases.

4. CHANGE IN TASTE AND FASHION:

it is affected by three factors

individuals likes and dislikes

you tend to buy more or less of commodity because your likes and dislikes tend to change

trends and fashion

you are influenced by emerging trends and fashion. you simply want to trendy accordingly your prefer to more of commodity.

climatic condition

your taste and preference tend to change in climatic environment. in winter there is more demand of tea and coffee while in summers cold drinks and ice creams are demanded more.

5.SIZE AND COMPOSITION OF POPULATION (N):

if size of population increases, there will be more requirements of goods and services, hence quantity demanded will be higher. composition of population determines the types of consumer goods demanded. i.e. baby related goods, young or old related goods . if old people are increasing demand for medicines will increases.

6.EXPECTED PRICE (E):

when the expected price of a commodity is higher than the market price, the consumer prefer to demand early, hence in this case quantity demanded increases. when the expected price is likely to be less than the market price, the consumer prefer to postpone the demand , hence quantity demanded decreases.

7. DISTRIBUTION IF INCOME (YD):

market demand is influenced by distribution of income. if income is equally distributed demand for commodity is expected to high. if income is not equally distributed demand for a commodity ie expected to low.

8.GOVERNMENT POLICIES :

favorable government policies leads to increase on demand and vice versa. when government policies are favorable then government gives subsidies therefore p[rice decrease and demand increase. due to unfavorable policies government impose taxes therefor price increase and demand decreases.

9.SEASON AND CLIMATE :

favorable season and climate leads to increase in demand and vice versa. in winters demand for woolen garments will increase and in summers demand for ice cream will increase.

10. ECONOMIC FLUCTUATIONS:

if a economy passing through a period of boom there will be increase in demand and vice versa .

DEMAND FUNCTION

it expresses relationship between demand of a commodity and various factors affecting it .it is of two types

individual demand function

it shows the demand of a commodity by an individual consumer in the market and its various determinants

D=F(P,Pr,Y,T,E)

D = demand of a commodity

F = function

P = price of a commodity

Pr = price of related goods

Y = income of consumer

T = taste of consumer

E = expectations

market demand function

it shows the relationship between market demand of a commodity to various determinants:

D =F(P,Pr,Y,T,E,N,S,G,YD)

D =demand of a commodity

F = function

P = price of a commodity

Y =income

Pr = price of related goods

T =taste and preferences

E = expectations

N = population

S = season and climate

g = government policy

Yd = distribution of income

law of demand

others things being equal when with the increase in price demand decrease and with the fall in price demand increases i.e. there is a inverse relationship between price and demand i.e. law of demand.

dx = f (PX) cetris paribus

Dx = demand of 'x' commodity

px = price of 'x' commodity

assumptions of the law

i) no change in income of consumer

ii) no change in population

iii) no expectations regarding future change in price of commodity

iv) no change in price of related goods

v) no change in government policy

vi) no change in season and climate

vii) no change in distribution of income

viii) no change in fashion and taste

EXPLANATION OF THE LAW

i) demand schedule

ii) demand curve

meaning of demand schedule

it is schedule in which others things remaining the same express the relationship between different amounts of commodity demand at different prices.

it is of two types

i) individual demand schedule

ii) market demand schedule

meaning of demand schedule

it shows demand of an individual consumer in the market at different prices and others things being equal.

price demand

1 50

2 40

3 30

4 20

5 10

its clear from the table that when price increases from Rs 1 to 2, 3, 4, 5 demand decreases from 50 to 40, 30, 20, and 10.

market demand schedule

it shows demand of all consumers in the market at different prices for this its assumed that there are 2 consumers in the market i.e. A and B and by joining their demand market demand is obtained.

market demand =A'SD + B'SD

price of commodity A's demand B's demand market demand

1 50 60 50+60= 110

2 40 50 40+ 50= 90

3 30 40 30+40= 70

4 20 30 20+30= 50

its clear from the table that as price increases from Rs 1 to 2, 3, 4, 5 market demand decreases from 110 to 90, 70, 50.

B. demand curve

it is a graphic presentation of demand schedule expressing the relation between different quantities at different prices.

i) individual demand curve

the graphic presentation of individual demand schedule is called individual demand curve.

its clear from the diagram the demand curve is sloping downward that is inverse relationship between price and demand.

ii) market demand curve

the graphic presentation of market demand schedule is called market demand curve.

in the diagram i) A's demand, AA is sloping downward. in the diagram ii)B's demand curve BB and in the diagram iii) market demand curve MM is slopind downward.

causes of operation of law of demand or causes of downward sloping demand curve

there is inverse relationship between price and demand i.e. with increase in price demand falls and with the decrease in price demand increase. as shown in the diagram

the following are the causes of downward sloping demand curve

1. LAW OF DIMINISHING MARGINAL UTILITY: according to this law as the consumer in a given time increases the consumption of a same commodity, the utility from each successive unit goes on diminishing. therefore, the consumer will buy more and more units of commodity only when he has to pay less and less price for each success unit, that's why he will demand more at less price.

2.CHANGE IN NO. OF CONSUMERS

when the p[rice of commodity falls some new consumer enter into the market therefore demand increases. on the other hand when price of commodity increases some old consumers will exit the market and therefore demand will decreases.

3. SUBSTITUTION EFFECT :

an increase in price of the commodity say pepsi also means that price of its substitutes say coke has fallen in relation to that of pepsi even though the price of coke remains unchanged. so people will buy more of coke and less of pepsi .this is called substitution effect.

4.INCOME EFFECT:

a fall in price leads to increase in real income of consumer with the result that he buys more when price falls . similarly increases in price leads to fall in real income and as a result demand falls.

5.DIFFERENT USES OF A COMMODITY:

a commodity having different uses is generally used at for large scale for e.g. milk is used for tea, coffee, curd, cheese etc. if price of milk goes up its consumption ids restricted to very important uses say teas consequently demand for milk falls which proves that with the increase in price demand falls.

EXCEPTIONS OF THE LAW OF DEMAND

1. IGNORANCE OF CONSUMER : if consumer is not aware of competitive price of commodity he may purchase more of commodity at higher price it may also he due to thinking of consumer that high price commodities are alwats superior.

2. COSTLY ITEMS OR ARTICLE OF DISTINCTION OR PRESTIGE GOODS: these are those goods which are purchased by rich people to distinguish them from poor people such as diamond sets, costly carpets, cars etc. demand of those commodities increase with increase in price.

3. CHANGE IN FASHION TASTE AND PREFERENCES: such change in behaviors of consumer are also responsible for making law of demand ineffective.

4. GIFFEN GOODS: these are low quality goods such as coarse grains. coarse wheat etc. in case of such goods when price falls demand falls because people start purchasing superior brands of commodity with extra purchasing power, therefore in this case demand curve is positively sloping.

5.BASIC NECESSITIES OF LIFE: there are certain basic necessities of life such as salt, sugar etc. in case of such goods demand of commodity remains the same irrespective of change in price.

MISCELLANEOUS FACTORS

if others factors affecting demand change, the law of demand fails.

change in demand

meaning of change in quantity demanded:

when demand changes due to change in price that is called qty. demanded.

its of 2 types

1. EXTENSION DEMAND:

others thing being equal with fall in price demand extends is called extension in demand

price demand

5 1

1 5

its clear from the table that when price falls from Rs5 to 1 demand extends from 1 unit to 5 units. in the diagram downward/forward rightward movement along the same demand curve A to B is showing extension of demand.

2. contraction of demand

others thing being equal, when with the increase in price demand falls that is called contraction of demand.

price demand

1 5

5 1

it is clear from the tables that when price increase from Rs 1 to Rs 5, then demand falls from 5 to 1 unit. in the diagram upward movement along the same demand curve from point B to A is showing contraction of demand.

difference between extension and contraction of demand

extension of demand contraction of demand

cause it is caused by fall in price it is caused by increase in price

price demand price demand

5 1 1 5

1 5 5 1

movement : there is a downward movement : there is an upward

movement along the same curve. movement along the same curve.

change in demand

when demand changes due to factors other than price i.e. called change in demand. it is of two types.

i) increase in demand

ii) decrease in demand

increase in demand

when demand increases due to factors other than price i.e. increase in demand. it is explained in two ways.

1. same price more demand

when at the same price, more quantity is demanded i.e. called increase in demand.

price demand

3 3

3 4

it is clear fro m the table remaining the price same i.e. 3 Rs. demand increases from 3 to 4 unit. in the diagram right side/ upward forward shifting of demand curve from DD to D1D1 is showing increase in demand.

2. same price same demand

when at the more price is same qty. is demanded i.e. also called increase in demand.

price demand

3 3

4 3

it is clear from the table that when price increases from 3 to 4 Rs demand remains the same i.e. 3 units. in the diagram right side shifting/ forward shifting/ upward shifting/ of demand curve from DD to D1D1 is showing increase in demand.

causes of increase in demand

causes of right side shifting of demand curve

1. increase in income of consumer

2. increase in wealth of consumer

3. when taste and preference shift in favor of commodity

4. when price of commodity is expected to increase in near future.

5. increase in no. of consumer

6. when price of substitute good increase

7. when price of complementary good falls

decrease in demand

when demand decrease due to factors other than price is that is called decrease in demand.

explanation

ii is explained in 2 parts

2. same price less demand

when at the same price less qty. demanded that is called decrease in demand.

price demand

3 3

3 2

it is clear from the table that remaining the price same demand decrease from 3 units to 2 units.

in the diagram left side/ backward shifting of demand curve from dd to d1d1 is showing decrease in demand..

2. less price same demand :

when at the less price same qty. is demanded i.e. called decrease in demand

price demand

3 3

2 3

it is clear the diagram that left side/ backward/ downward/ shifting of demand curve from DD to D1D1 is showing decrease in demand.

causes of decrease in demand

or

left side shifting of demand curve

1. decrease in income of consumer

2. decrease in wealth of consumer

3. when taste and preferences shift against the commodity

4. when price of commodity is expected to decrease in near future

5. decrease in no. of consumer in the market

6. when price of substitute goods decreases

7. when price of complementary goods increases

Subscribe to:

Comments (Atom)